信贷违约预测实战:从数据清洗到XGBoost调优全流程

文章目录

信贷违约预测实战:从数据清洗到XGBoost调优全流程一、项目背景二、数据探索与预处理1. 数据加载与基础检查2. 特征清理

三、数据与特征处理四、构建模型五、XGBoost调优实战1.基础参数设置2. 贝叶斯优化调参3. 最佳参数4. 最终模型评估

六、完整代码仓库

一、项目背景

精准预测用户贷款违约风险是风控系统的核心。本文将带您完整复现一个信贷违约预测项目,从数据清洗、特征工程到模型调优,最终实现高精度预测。项目使用Python,基于天池信贷数据集,全程手把手教学。

二、数据探索与预处理

1. 数据加载与基础检查

import pandas as pd

import numpy as np

读取数据,删除无关列

df = pd.read_csv('data/train.csv').drop(['id', 'issueDate'], axis=1)

检查数据基本信息

# 数据基本信息探索

df.info()

df.describe()

df.dtypes.value_counts()

# 找出有缺失值的特征

df.isnull().sum()

# 缺失值比例

df.isna().mean()

关键发现:

20列含缺失值(最高缺失率5.8%:employmentLength)4列非数值型(grade, subGrade, employmentLength,earliesCreditLine)policyCode列值无变化,需删除,n11,n12列类似,需删除

2. 特征清理

删除无用特征

df = df.drop(columns=['policyCode', 'n11', 'n12'])

处理earliesCreditLine列,提取年份

df['earliesCreditLine']=df['earliesCreditLine'].apply(lambda s: int(s[-4:]))

三、数据与特征处理

可以通过业务经验或者金融相关知识构建一些新特征或者交互项等,由于篇幅有限,这里不再赘述,希望大家发挥主观能动性!!!

# 自变量与因变量分离

y=df.pop('isDefault')

缺失值填充

类别型变量:用众数填充

cat_cols = ['grade', 'subGrade', 'employmentLength']

for col in cat_cols:

df[col].fillna(df[col].mode()[0], inplace=True)

数值型变量:用中位数填充

num_cols = df.select_dtypes(include=['float64', 'int64']).columns

for col in num_cols:

if df[col].isnull().sum() > 0:

df[col].fillna(df[col].median(), inplace=True)

类别型变量编码grade编码(A-G)

grade_map = {'A': 0, 'B': 1, 'C': 2, 'D': 3, 'E': 4, 'F': 5, 'G': 6}

df['grade'] = df['grade'].map(grade_map)

subGrade编码(按A1-A5, B1-B5…顺序)

subGrade_map = {}

for i, grade in enumerate(['A', 'B', 'C', 'D', 'E', 'F', 'G']):

for j in range(1, 6):

subGrade_map[f'{grade}{j}'] = i5 + j-1

df['subGrade'] = df['subGrade'].map(subGrade_map)

employmentLength编码(<1年=0, 1年=1…10+年=10)

emp_length_map = {

'< 1 year': 0, '1 year': 1, '2 years': 2, '3 years': 3, '4 years': 4,

'5 years': 5, '6 years': 6, '7 years': 7, '8 years': 8, '9 years': 9,

'10+ years': 10

}

df['employmentLength'] = df['employmentLength'].map(emp_length_map)

编码逻辑:

grade:A(0) < B(1) < C(2) < … < G(6)

subGrade:A1(0), A2(1), …, A5(4), B1(5), B2(6)… G5(34)

employmentLength:按年限升序映射

四、构建模型

from sklearn.model_selection import train_test_split,StratifiedKFold

from sklearn.linear_model import LogisticRegression

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

from xgboost.sklearn import XGBClassifier

from lightgbm import LGBMClassifier

from sklearn.metrics import classification_report,roc_auc_score

判断因变量是否类别平衡

y.value_counts()/y.count()

为XGBoost设置权重

scale_pos_weight = y.value_counts()[0] / y.value_counts()[1]

模型对比

models = {

'log_model': LogisticRegression(max_iter=5000,random_state=42),

'tree':DecisionTreeClassifier(random_state=42),

'RF':RandomForestClassifier( random_state=42),

'XGB':XGBClassifier(random_state=42),

'lgb':LGBMClassifier(random_state=42)

}

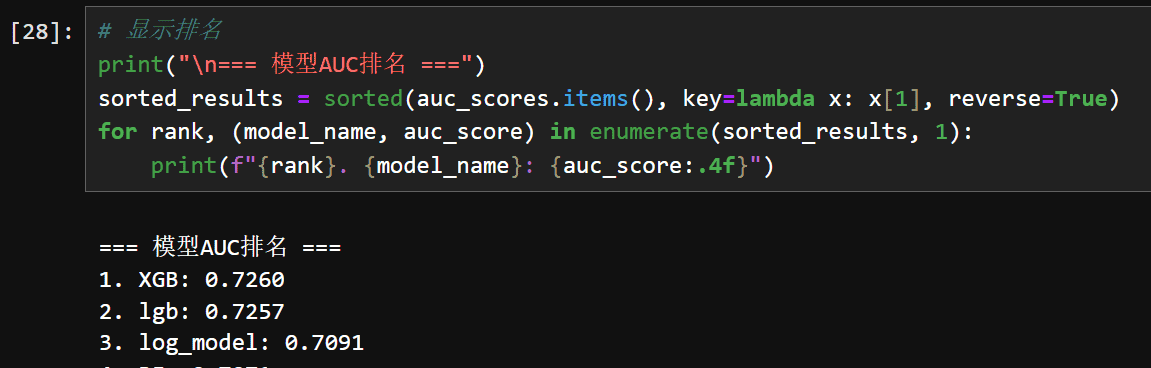

以auc为评估指标来判断模型性能

数据质量应该不太好,所以auc都不是很高,进一步构造特征等措施,auc提升的也不多。

结论:XGBoost表现最佳,选择其作为基础模型

五、XGBoost调优实战

1.基础参数设置

# XGBoost基础参数

xgb_base_params = {

'objective': 'binary:logistic',

'eval_metric': 'auc',

'tree_method': 'hist',

'n_jobs': -1,

'scale_pos_weight': scale_pos_weight,

'random_state': 42,

'verbosity': 0

}

2. 贝叶斯优化调参

from bayes_opt import BayesianOptimization

def xgb_cv(n_estimators, max_depth, learning_rate,min_child_weight, subsample, colsample_bytree, gamma, reg_alpha, reg_lambda):

params = {**xgb_base_params,

'n_estimators': int(n_estimators),

'max_depth': int(max_depth),

'learning_rate': learning_rate,

'subsample': subsample,

'colsample_bytree': colsample,

'scale_pos_weight': scale_pos_weight,

'objective': 'binary:logistic',

'random_state': 42,

'gamma': gamma,

'reg_alpha': reg_alpha,

'reg_lambda': reg_lambda

}

#3折交叉验证

scores = []

for train_idx, val_idx in StratifiedKFold(3).split(X_train, y_train):

X_train_fold, X_val_fold = X_train.iloc[train_idx], X_train.iloc[val_idx]

y_train_fold, y_val_fold = y_train.iloc[train_idx], y_train.iloc[val_idx]

model = XGBClassifier(params)

model.fit(X_train_fold, y_train_fold)

scores.append(roc_auc_score(y_val_fold, model.predict_proba(X_val_fold)[:, 1]))

return np.mean(scores)

定义搜索空间

pbounds = {

'n_estimators': (100, 500),

'max_depth': (3, 10),

'learning_rate': (0.01, 0.3),

'subsample': (0.6, 1.0),

'colsample': (0.6, 1.0)

}

执行优化

optimizer = BayesianOptimization(f=xgb_cv, pbounds=pbounds, random_state=42)

optimizer.maximize(init_points=10, n_iter=20)

3. 最佳参数

# 获取最佳参数

xgb_best_params = {**xgb_base_params}

xgb_best_params.update(xgb_optimizer.max['params'])

xgb_best_params['n_estimators'] = int(xgb_best_params['n_estimators'])

xgb_best_params['max_depth'] = int(xgb_best_params['max_depth'])

print("XGBoost最佳参数:")

for k, v in xgb_best_params.items():

print(f" {k}: {v}")

4. 最终模型评估

训练最终模型

final_model = XGBClassifier(

**xgb_best_params,early_stopping_rounds=50)

final_model.fit(X_train, y_train,

eval_set=[(X_val, y_val)],

verbose=False)

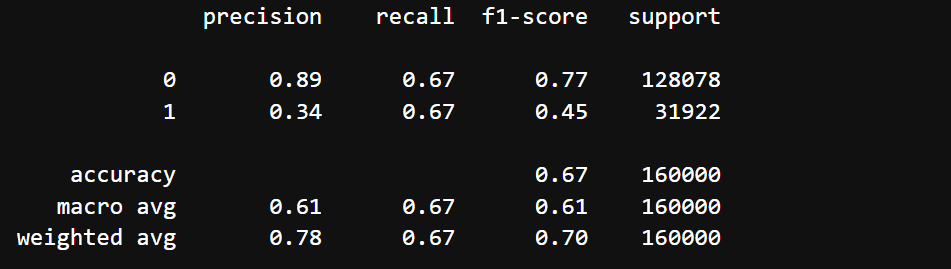

#测试集评估

print(classification_report(Ytest, final_model.predict(Xtest)))

print("AUC: ", roc_auc_score(Ytest, final_model.predict_proba(Xtest)[:, 1]))

最终结果:

六、完整代码仓库

GitHub项目地址(含完整Jupyter Notebook)

本文数据集已脱敏处理。

欢迎在评论区讨论:

“在实际业务中,您认为哪些特征对违约预测最关键?”

“如何平衡模型精度与业务可解释性?”

暂无评论内容